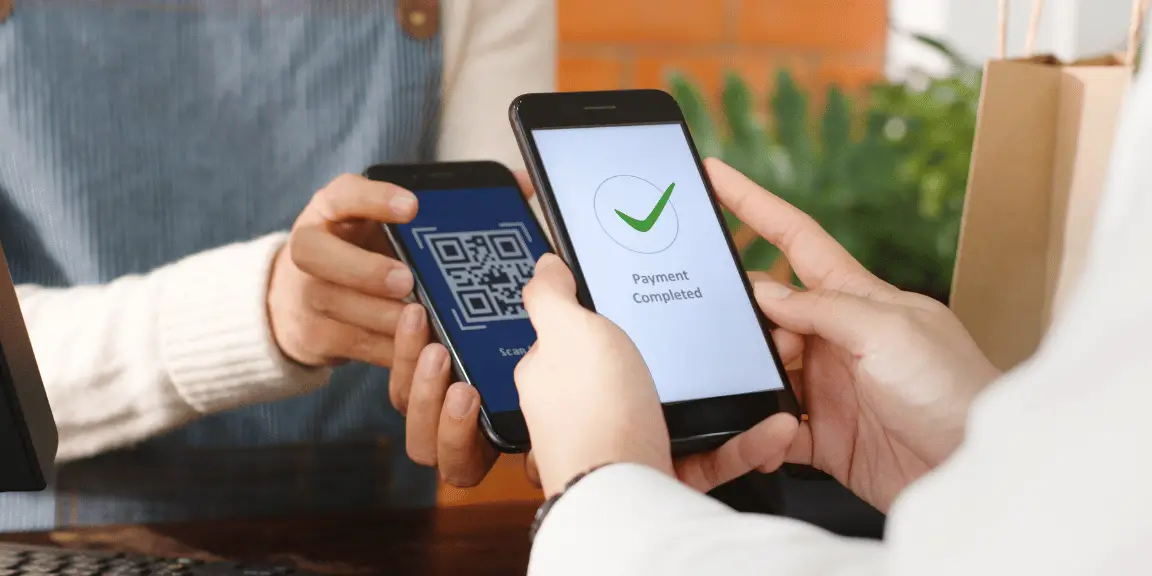

5 Advancements in Payment Technologies That Retailers Should Know About

Back in 1984, Westpac was the first of the big four banks in Australia to introduce an EFTPOS system, which they did at several BP petrol stations around the country. Fast forward forty years, and this payment technology is now in over 440,000 retailers in the country, thanks to products like Smartpay’s EFTPOS machines.

For many consumers, it is the preferred way to pay for their purchases. However, in recent years a number of other payment technologies have emerged, which might test their loyalty.

In this post, we’ll take a look at 5 advancements in payment technologies that retailers should know about. It doesn’t matter if you run a major supermarket, a funky boutique clothes shop or just a plain old small business, these innovations may well be relevant to your business.

1. Advances in Security for Contactless Payments

The days of buying things with cash could well be numbered. According to a report by the RBA, around 95% of Aussies prefer to pay for their in-person purchases via contactless payments.

While most people recognise the benefits of contactless payments – namely convenience, speed and efficiency – which results in less waiting times at the checkout, they might not be aware of how much the security aspects of it have improved.

Today, technologies like tokenization are incorporated within them to safeguard against sensitive data being compromised during the payment process. Therefore, it now adds a stronger layer of protection against fraudulent activity.

2. Increasing Use of BNPL (Buy Now Pay Later)

In recent years, the system of BNPL (Buy Now Pay Later) has become very popular among consumers.

Offered by providers like Zip and Afterpay, this technology allows consumers to pay for their purchases at a later time, typically over four equal payments scheduled 2-4 weeks apart. Therefore, if someone wanted to buy a pair of shoes for $200, they could do so over four different $50 instalments.

As this option does not involve accruing interest, it is a much more attractive proposition to credit cards. Not only does it reduce the risk of customers falling into debt, but it can also enable them to get a better handle on their cash flow.

Retailers can enjoy benefits from BNPL as they can provide their customers with more flexible payment methods, which should result in increased sales. Crucially, they should also get paid immediately from the service providers.

3. PaaP (Payment as a Platform)

PaaP, or Payment as a Platform, is an innovative approach that has transformed payment services into versatile platforms.

It enables third parties to offer their products or services seamlessly through payment apps, therefore providing their customers with a much more user-friendly experience.

PaaP also allows retailers to cash in on the mobile money market in emerging economies, where mobile transactions are rapidly growing. It facilitates the smooth integration of services like e-commerce, loyalty programs and fulfilment into the payment platforms.

The ultimate benefit of PaaP is that it enhances customer experience by streamlining routine transactions through increased efficiency, improved functionality and incredible convenience for retailers and customers.

4. Emergence of AI in enhancing payment methods

Over the last 12 months, the concept of Artificial Intelligence has gained widespread recognition thanks to technologies like ChatGPT. However, it has also been instrumental in driving payment innovation across various industries, including retail.

Systems that are AI-powered can process and analyse massive volumes of data. Subsequently, they have been able to refine how transactions are processed, managed and personalised.

They have even been able to make them more secure as they can predict and prevent targeted cyberattacks on any given payment ecosystem. Hence, as a retailer or a customer, you are much better protected now than ever before.

5. Cryptocurrencies

It might surprise you to learn that cryptocurrency such as Bitcoin and Ethereum are becoming genuine methods of payment in the retail industry.

Indeed, companies like KFC, Subway, Pizza Hut, Whole Foods and Starbucks currently do, or have, accepted them as a payment option in various parts of the world. Additionally, several smaller retailers such as Curryupnow.com in San Francisco, The Pink Cow, a cafe in Japan and the Old Fitzroy, a pub in Sydney, also recognise them as legal tender.

While this might not be a predominant payment method for years to come, there is a distinct possibility that an increasing number of retailers will embrace this method of payment in the future.

How Cash Flow Financing Can Transform Your Business Operations

In the landscape of small business, cash flow is a crucial advantage. Without a healthy flow of capital, even the most revolutionary business ideas and the hardest-working entrepreneurs will flounder. Cash flow finance provides a much-needed solution to what can often be the most pressing issue in business development.

In this comprehensive guide, business owners and entrepreneurs will learn how to leverage cash flow finance to remove barriers to growth, increase operational flexibility, and take advantage of new opportunities — all while avoiding the potential pitfalls that come with traditional financing routes.

Understanding Cash Flow Financing

Cash flow financing, also known as cash flow loans, is a type of financing designed to bolster the working capital of a business. Unlike traditional term loans, cashflow finance is not necessarily tied to a specific purchase or investment but seeks to address ongoing operational needs.

These loans are meant to help businesses that already have a strong revenue stream and may experience temporary shortfalls due to issues such as seasonality, slow-paying customers, or unexpected expenses.

Who Can Benefit from Cash Flow Financing?

Entrepreneurs who have good revenue but who are limited by cash flow can use this form of lending to bridge the gap. It is particularly powerful for:

Seasonal businesses with fluctuating income

Startups without a well-established credit history

Businesses looking to seize immediate growth opportunities

Companies with long accounts receivable cycles

Businesses recovering from a short-term setback

Cash flow financing is not just for companies in financial distress; it is a strategic tool for any business wanting to grow and improve their operations.

Navigating Cash Flow Challenges in Operations

Cash flow problems can be a thorn in the side of even the most profitable business. They arise due to a multitude of factors, many of which are commonplace in the business world. By recognizing these challenges and addressing them with the appropriate financing techniques, business owners can maintain stability in their operations and ensure they are well-positioned to grow.

Understanding the Causes of Cash Flow Concerns

There are several common culprits for cash flow issues:

Seasonal fluctuations: Businesses with seasonal cycles may experience periods of high demand and revenue followed by lulls.

Large inventory purchases: Maintaining substantial stock to meet customer demand can tie up a significant portion of available capital.

Slow-paying clients: Delayed payments from customers can disrupt cash flow, especially if the business does not have savings to cover the gap.

Utilizing Cash Flow Financing Solutions

To tackle these challenges, businesses can utilize a range of cashflow finance solutions, such as:

Invoice financing: This method involves using unpaid invoices as collateral to obtain a loan, which can provide immediate cash to address short-term needs.

Revolving lines of credit: These credit lines are pre-approved by lenders and can be tapped into as needed, providing a flexible source of working capital.

Short-term loans: Sometimes a temporary cash injection is all that is needed to overcome an obstacle, and short-term loans can offer a quick fix for cash flow problems.

Leveraging Cash Flow for Expansion and Investment

The ability to capitalize on growth opportunities is a hallmark of successful business strategies. With cashflow finance, businesses can position themselves to take advantage of expansion plans and investments that may otherwise be outside their reach.

Financing Growth Strategies

Expanding into new markets: Whether it involves new territories or online platforms, expanding the customer base requires investment.

Acquiring new equipment or technology: Keeping operations efficient and up-to-date is essential in the modern business environment.

Hiring and training new staff: A growing business needs a growing team, which necessitates adequate resources for recruitment and training.

The Benefits of Cash Flow Financing

By financing expansion through cash flow, businesses can enjoy several benefits over traditional loans, including:

Greater flexibility: Decisions on how to allocate loan proceeds are entirely at the discretion of the business, offering more flexibility than tied-up bank loans.

Faster access: Unlike traditional bank loans, cashflow finance options typically have a faster application and approval process, giving businesses quicker access to the capital they need.

Less risk: Because cash flow financing is based on existing cash flow, it is often less risky for businesses, particularly those without hard assets to secure a loan against.

Avoiding Cash Flow Pitfalls and Missteps

While cash flow financing can be a lifeline for many businesses, it is not without its challenges. Business owners must approach this type of financing with a clear strategy and understanding of the potential risks involved.

Common Cash Flow Financing Mistakes

Relying on financing as a crutch: While it’s important to address immediate cash flow needs, businesses should not become over-reliant on financing as a long-term solution.

Not thoroughly researching options: There are various cash flow financing options available, and not all will suit every business’s needs. Understanding the terms and costs of different options is crucial.

Failing to forecast future cash flows: Business owners should have a clear picture of their future financials to ensure they can comfortably meet their repayment obligations.

Making the Most of Cash Flow Financing for Your Business

Taking control of your business’s cash flow is a pivotal step toward ensuring its success. Cash flow financing offers a unique opportunity to transform the way businesses handle their financial needs, providing a buoyant approach to operations that can carry them from strength to strength.

Crafting a Strong Cash Flow Financing Strategy

To make the most of cash flow financing, businesses should develop a comprehensive strategy that aligns with their long-term goals, leverages financing to maximize potential growth, and builds in contingencies for unexpected cash flow hiccups.

The Long-Term Impact of Cash Flow Financing

Well-managed and strategic use of cash flow financing can have a profound impact on a business’s trajectory, enabling it to weather storms, seize opportunities, and continually improve its standing in the marketplace.

From Purchase to Decommissioning: Mapping Out Asset Lifecycle Stages

In today’s changing business environment, companies are always looking for ways to get the most out of their resources while keeping costs down. To achieve this, organizations need to have a grasp of how to manage their assets throughout their lifecycle. Starting from when they are first acquired to when they are retired, understanding each stage in the asset lifecycle is key to achieving peak performance and cost-effectiveness. In this article, we’ll take a look at each stage, discussing the best practices and common pitfalls.

Procurement/Obtaining

The initial phase of asset lifecycle management is procurement or obtaining. During this stage, it’s important for organizations to carefully consider their needs and objectives in order to make informed purchasing decisions. It’s wise to explore options in the market while taking into account factors like quality, reliability, return on investment (ROI), and the reputation of vendors.

Avoid rushing into a purchase based on price; instead, focus on assessing the long-term value and productivity enhancements that align with your organization’s objectives. Involving stakeholders can offer perspectives that contribute to shaping a successful procurement strategy.

Implementation/Deployment

After assets are acquired, it’s time for the implementation or deployment phase. Proper installation is crucial in ensuring that assets operate at their right from the start. Businesses frequently rely on the expertise of manufacturers and hire skilled professionals to install specific types of equipment.

When implementing these assets, organizations must take into account factors like compatibility with existing systems and adherence to industry standards and regulations related to equipment safety and reliability.

Regular Maintenance and Monitoring

Following installation, it is crucial to conduct maintenance and monitoring to ensure the performance of the assets over their lifespan. This involves tasks such as servicing components based on manufacturer recommendations, establishing maintenance schedules, regularly inspecting for signs of wear and tear, and accurately calibrating equipment.

Failure to prioritize maintenance can lead to decreased productivity, unexpected downtimes, and higher repair expenses. By adopting a maintenance approach and monitoring potential issues, they can be identified early for timely resolution.

Upgrades and Enhancements

Given the pace of advancements, businesses often need to upgrade their assets to stay competitive and aligned with current trends. Assessing the performance of an asset in relation to evolving business requirements is key in determining upgrades or enhancements.

Options for upgrades may include software updates, hardware improvements, or the implementation of automation systems. It is important to evaluate the cost-effectiveness of each upgrade against productivity gains.

Disposal/Decommissioning

The final phase of an asset’s life cycle involves its disposal or decommissioning. It is important to plan the retirement of assets to minimize impact and make efficient use of resources.

Adhering to regulations and disposal methods can help avoid issues and safeguard the reputation of a brand. Depending on the type of asset, considerations may include protocols for data destruction recycling efforts, exchanging with vendors that promote sustainability, or facilitating equipment donations.

Risk Assessment and Mitigation

Throughout the life cycle of assets, organizations need to assess risks, identify vulnerabilities, and implement mitigation strategies. This phase involves assessing external risks that could affect asset performance, reliability, or security.

Internal risks might involve factors like training, limited maintenance budgets, or human errors; external risks could include regulation changes, supply chain disruptions, or cybersecurity threats. Conducting risk analysis enables organizations to establish plans and implement measures for effective risk mitigation.

Data Management and Documentation

Data management and documentation are underestimated yet crucial aspects of an asset’s life cycle. Keeping track of details about assets, such as warranties, service history, upgrades/updates installed, and any incidents or challenges encountered, plays a role in aiding effective decision-making throughout the lifespan of the asset.

By following data management procedures, it is possible to minimize delays in troubleshooting tasks or performance evaluations. Maintained documentation enables teams to streamline support processes by accessing historical data essential for making informed decisions.

Conclusion

Efficiently managing an asset’s lifecycle is vital for companies aiming for profitability while minimizing costs. Breaking down each phase, from acquisition to disposal, equips organizations with the ability to make choices that enhance productivity. By incorporating the best practices and steering clear of pitfalls, businesses can optimize their asset investments and stay competitive in todays ever changing market environment.

From Vision to Viability: Securing Your Business’s Tomorrow, Today

Turning a vision into a sustainable and profitable business demands more than just passion and hard work. It requires a strategic approach to planning, an understanding of the market, and a keen eye for risk management. Every successful entrepreneur knows that the viability of their business hinges on their ability to anticipate changes, adapt to challenges, and make informed decisions.

This article aims to guide small business owners through the essential steps of transforming their initial business idea into a resilient, thriving enterprise. By focusing on core strategies that fortify a business against the unpredictable tides of the market, we will delve into how to secure your business’s tomorrow, today.

The Foundation of Your Vision: Exploring the Core of Your Business Idea

Navigating the initial stages of launching a business is a challenging endeavor, underscored by statistics indicating the precarious nature of new ventures. Research from the Bureau of Labor Statistics, highlighted by Fundera, reveals a sobering trajectory for small businesses: about 20% do not survive past their first year. As time progresses, the survival rate diminishes further, with 30% closing by the end of the second year. The five-year mark proves even more pivotal, as approximately 50% of businesses will have ceased operations. Looking a decade out, the landscape becomes even more stark, with a mere 30% of businesses managing to sustain, translating to a 70% failure rate over ten years.

This data underscores the critical importance of laying a robust foundation for your business. A clear, compelling vision is not merely aspirational; it serves as the bedrock upon which successful businesses are built. It’s not only about the products or services you intend to offer but also about understanding the unique value your business brings to the marketplace. Who is your target customer, and what specific needs or challenges will your business address? Achieving clarity around these questions is crucial for carving out a distinct space in a competitive environment. It informs strategic decision-making across all facets of the business, from marketing to product development to customer engagement, ensuring that each step forward is in service of a cohesive, overarching goal. Establishing this solid foundation is essential for not just surviving but thriving in the challenging landscape of business ownership.

Market Trends and Forecasting: Aligning Your Business with Future Opportunities

Staying ahead in today’s business environment means being able to swiftly navigate through market trends and forecast future opportunities. This alignment is crucial for the longevity and relevance of your business. It involves analyzing current market conditions, customer behaviors, and technological advancements to predict where your industry is headed.

By staying informed, you can adapt your business model to meet upcoming demands and seize opportunities before they become mainstream. This proactive approach not only keeps your business competitive but also positions it as an industry leader. Additionally, understanding and anticipating market trends can help you make smarter investments in marketing, product development, and operational efficiencies, ensuring that your business remains viable and vibrant in the face of changing market dynamics.

Planning for the Unexpected: The Importance of Being Prepared

Preparing for unforeseen events is vital for the stability and longevity of any business. Insurance plays a significant role in this preparation, providing a safety net that can help businesses recover from financial losses due to accidents, natural disasters, lawsuits, and other unforeseen circumstances. According to The Hartford, a leading provider of business insurance, the costs associated with various insurance policies for small businesses average as follows:

Business Owner’s Policy (BOP): This comprehensive policy combines general liability insurance and property insurance, usually at a cost advantage. The average annual premium is $3,125, with an average monthly premium of $261.

General Liability Insurance (GLI): Essential for protecting against claims of bodily injury, property damage, and advertising injury, the average annual premium for GLI is $1,057, translating to about $88 per month.

Workers’ Compensation Insurance: This insurance covers medical costs and a portion of lost wages for employees who become injured or ill on the job. The average annual premium stands at $840, or approximately $70 per month.

These figures underscore the importance of allocating resources towards comprehensive insurance coverage. By investing in the right insurance policies, businesses can protect themselves against significant financial and operational setbacks, ensuring that they can continue to thrive even in the face of unexpected challenges. Proper planning and preparedness, underpinned by adequate insurance, are indispensable components of securing a business’s future.

Risk Management Essentials: Identifying and Mitigating Business Risks

Risk management is a crucial aspect of ensuring the viability of any small business. Identifying potential risks before they manifest allows business owners to implement strategies to either avoid these risks entirely or minimize their impact. Risks can range from financial uncertainties, legal liabilities, management errors, accidents, and natural disasters to market fluctuations. A comprehensive risk assessment should be the first step in any risk management plan. This involves analyzing internal operations, industry-specific risks, and external factors that could affect the business.

Following this, developing a risk management plan that includes steps such as purchasing appropriate insurance, creating operational redundancies, and establishing strong health and safety protocols is essential. Regularly reviewing and updating risk management plans ensures that the business remains prepared for potential challenges, safeguarding its future and ensuring steady growth.

Financial Planning for Longevity: Strategies to Ensure Economic Resilience

Financial planning is the backbone of a business’s longevity and economic resilience. It’s about more than just keeping the books balanced; it’s about strategizing for future growth while preparing for potential downturns. Effective financial planning involves several key practices: accurate financial forecasting, prudent cash flow management, and strategic investment in growth opportunities. Forecasting helps businesses anticipate financial challenges and opportunities, allowing for proactive adjustments to spending and saving strategies.

Cash flow management, including monitoring receivables and payables closely, ensures that businesses can meet their obligations on time and remain solvent. Lastly, investing in growth opportunities must be balanced with the need for financial stability, requiring a careful analysis of potential returns versus risks. By adhering to these principles, businesses can build a financial foundation strong enough to support both current operations and future ambitions, ensuring they remain competitive and can navigate the uncertainties of the business world.

The Role of Technology in Business Sustainability: Embracing Digital Solutions

Embracing digital solutions allows businesses to operate more efficiently, reach new markets, and offer innovative products or services. Technology can streamline operations, from automating routine tasks to enhancing data analysis for better decision-making. Digital marketing platforms expand a business’s reach, enabling them to engage with customers across the globe.

E-commerce capabilities allow businesses to sell products and services online, opening up new revenue streams. Moreover, technology can foster sustainability by enabling remote work, reducing the need for physical office space, and lowering travel-related carbon emissions. However, adopting technology also requires careful planning to ensure cybersecurity and data privacy. By thoughtfully integrating technology into their operations, businesses can achieve greater efficiency, enhance customer satisfaction, and position themselves for long-term success in an increasingly digital world.

Building a Strong Brand and Customer Loyalty: The Keys to Competitive Advantage

The economic efficiencies of customer retention versus acquisition are striking, serving as a potent reminder of the value inherent in building a strong brand and fostering customer loyalty. It is widely recognized that attracting new customers can be significantly more expensive—by a factor of five to ten times—than the costs associated with selling to existing customers. This discrepancy highlights the substantial investment required to reach and convert new prospects compared to leveraging established relationships. Furthermore, those who have already engaged with your business tend to be more valuable over time, spending an average of 67% more than new customers. This increased spending reflects a deepened trust and familiarity with your brand, underscoring the importance of nurturing these existing relationships.

Building a strong brand and cultivating customer loyalty are therefore indispensable strategies for gaining a competitive advantage. By focusing on delivering exceptional value, quality, and customer service, businesses can encourage repeat business and foster a loyal customer base. This loyalty not only translates to increased revenue per customer but also enhances the overall brand reputation, making it easier to attract new customers through positive word-of-mouth and referrals. In this way, investing in your brand’s strength and customer loyalty is not just about retaining your current customer base—it’s a comprehensive strategy that impacts every aspect of your business’s growth and sustainability.

Securing Your Business’s Future: Next Steps in Your Entrepreneurial Journey

Securing the future of your business is an ongoing process that demands foresight, adaptability, and a commitment to continuous improvement. As your entrepreneurial journey progresses, the steps you take today lay the groundwork for tomorrow’s success. This means not only reflecting on the lessons learned from the past but also looking ahead to anticipate new challenges and opportunities.

To fortify your business for the future, it’s essential to remain vigilant about market trends and technological advancements, ensuring that your business adapts and evolves to stay relevant. Staying connected with your customer base, soliciting feedback, and being responsive to their needs will help you maintain a competitive edge. Furthermore, investing in your team’s development through training and fostering a culture of innovation can drive your business forward.

Financial health remains a cornerstone of business sustainability. Regularly reviewing your financial strategy, diversifying your income streams, and maintaining a prudent approach to spending and investment can safeguard your business against unforeseen economic fluctuations.

Lastly, building strong networks and partnerships can provide valuable support and opportunities for growth. Whether through industry associations, local business communities, or strategic alliances, these relationships can offer resources, advice, and collaboration opportunities.

As you navigate the next steps in your entrepreneurial journey, remember that the path to securing your business’s future is not linear. It requires a dynamic approach, embracing change, learning from setbacks, and celebrating milestones along the way. Your vision, grounded in the strategies you implement today, will guide your business toward a prosperous and resilient future.

8 Key Decision to Make When Launching a Business

When you’re looking to launch a new business, there are many things to consider. The questions you ask and the decisions you make before you launch are critical, helping you identify core elements of the company and its structure that can position it for future success.

Here are some of the basic considerations entrepreneurs should factor into their planning before they open the doors.

1. Whether to Launch

This question is perhaps the most important one to answer: Should I start the business?

Answering that question is a multi-fold venture, with multiple layers and complexities.

You need to determine if you are fully committed to the work it takes to launch your own business. You need to be prepared emotionally, physically and financially for the journey.

Let’s consider the financial part. Until you have a steady income stream, you will need to rely on personal savings to cover your monthly expenses.

You also need to persevere in fine-tuning the products and services your company offers. You’ll need to face rejection and criticism along the way. However, a strong belief in what you are providing can go a long way towards success.

2. Do Your Research

Research is an important element of any small business. Your initial research should focus on three areas:

Markets

Customers

Competitors

Market Research

This research helps you understand the markets in which you choose to compete. It includes learning about the communities in which you look to sell, the business climate, potential locations, and the industry. What are the trends that are defining the market and industry? Where are they headed in the next 1, 3 and 5 years?

Customer Research

Who are you selling your products and services to? Knowing the likely customers for your company is essential, no matter what industry you’re in or selling B2B, B2C or B2BC.

You want to answer the question: Why will customers want or need my product or service? The answer can help you fine-tune what you offer and make sure that you are making the case for how your products and services can solve customer problems.

You should also build profiles of your customers based on shared demographics around age, gender, location, income and profession. These ideal customer profiles will help position not just what you sell, but also how you sell and market.

Competitor Research

You need to know who you’re up against. Competitor research helps you refine your pricing, pitch and messaging.

Understand who has market share where you want to sell. Then use that information to differentiate what you’re selling to make it more attractive to your customers.

3. Build a Business Plan

Any new business should spend the time constructing a well-thought-out business plan. The plan helps you answer core questions and is necessary if you’re looking to secure financing. Here are the core elements of a business plan:

Executive Summary. Includes your name, mission statement, company description, how your products and services benefit customers, description of products and services and financial overview

Company Description. Goes into more detail about the business purpose, how it helps or benefits others, details about the customers and their shared demographics, and the uniqueness of your products and services

Market Analysis. Here is where you will summarize the research you’ve done on the markets and competitors, including competitor names, offerings, and, where known, sales information and their customer demographics

Descriptions. More detail on your products and services, including the history and the purpose of each

Sales and Marketing. Your approach to selling, with detailed descriptions of the strategies, tactics and expected outcomes

Funding. If you are seeking bank funding or investors, here is where you lay out how much you will need, how the funds will be used over the next five years, the type of financing you’re seeking and your desired terms and conditions

Financial Analysis. Details on past results, if any, and five-year projections, with monthly or quarterly forecasts. Will include balance sheets if you’ve already started your business and other charts and graphs to illustrate your financials

4. Choose a Business Structure

Your business structure is the legal organizational type used to define your company. The business structure you choose will have an impact on how your company operates, the taxes you pay and the amount of liability exposure you have.

There are multiple business types to consider, but the most common among small businesses are a sole proprietorship or limited liability company (LLC).

Sole Proprietorship

This is the simplest business type. There’s no formal paperwork to file and as the sole owner, you are responsible for all the decisions the company makes.

A sole proprietorship is called a pass-through company for tax purposes. That’s because the profits, losses and deductions are passed through directly from the company to the owner’s individual income tax returns.

From a liability perspective, a sole proprietorship carries some risk. There are no legal protections for the owner and in the case of a court judgment against the company, creditors can come after the owner’s personal assets, including homes, cars and savings.

LLC

An LLC is the most popular business structure for small businesses. In an LLC, you have choices about how the company is managed, either by the owners directly or by hiring a manager to run the day-to-day operations.

Taxes work much like with a sole proprietorship, with tax factors passing through from the company to the owners’ tax returns.

From a liability perspective, an LLC is a far safer choice. Except in extreme cases of misconduct, the owners of an LLC are protected from personal liability and their personal assets are protected, too.

Forming an LLC does require paperwork, both to file originally and on an ongoing basis. Starting a business in states like Florida, for example, requires filing paperwork and ensuring that all your documents are correct. That’s why many small businesses turn to a trusted partner to file and manage the paperwork.

5. Establish Business Bank Account and Credit Card

Running a business means being professional in how you appear to customers, partners and vendors. One of the best ways to achieve that professionalism is to establish your company with a bank or other financial institution.

With a business bank account, you can gain credibility, with transactions conducted on accounts that share your business name. Blending the personal and professional finances is risky and can erode the credibility you’re seeking to establish.

LLCs and corporations (another business structure) are required to have separate business bank accounts.

A business credit card is another good way to gain credibility. And with a business credit card, you can begin building a credit score for your business that’s separate from your personal credit. This business credit score is important and can help you gain more favorable rates on loans and insurance policies.

6. Choose a Name

A professional business name is important to convey who you are and what you do. When filing an LLC, you will need to choose a legal name, which may be different from the name you use commercially, which is known as your “doing business as” or DBA name.

States have online databases where you can research potential legal and DBA names. You’ll also need to formally file your names so that others do not take them.

7. Develop Your Brand

How do you want to be seen by your customers and the public? Answering this question helps to define your corporate brand. The brand is your public persona, a way to convey what your business is about.

Brand elements include your name and logo, which is a visual representation of your company. It’s also about the fonts, colors and words you use in signage, a business card, advertisements and other materials to promote your business.

8. Find Advisors

You don’t need to answer all these questions by yourself. A trusted team of advisors is essential for any business leader. These perspectives, from experienced advisors, help you answer questions and frame next steps in the company’s growth.

The most common advisors to employ are:

Attorney. A lawyer can answer legal questions, draft contracts and partnership agreements, and review materials on your behalf

Accountant. An accountant helps track and analyze your finances, prepare balance sheets and financial materials, and advise on where to invest

Financial Advisor. As a business owner, you have important decisions to make about your future financial well-being, succession plans and how to invest your hard-earned income

Starting your own business is an exciting time. By planning and asking important, tough questions, you’ll be positioned for success.

Tax Considerations for eBay Sellers: Understanding Sales Tax, Income Tax, and Deductions

We get it; taxes can be pretty complicated. However, we’re here to make all these things a little bit easier for you. If you’re an eBay seller feeling overwhelmed by all the tax rules and what you need to do, you’ve come to the right place. So, let’s start right from the very beginning!

Introduction to Tax Obligations for eBay Sellers

When you sell on eBay, there are a few tax basics you need to know. First, sales tax. It’s the tax you might need to collect from buyers, depending on where they live. We’ll help you understand when and how to do this.

Then, there’s income tax. The money you make from selling items can affect how much you owe in taxes, and we’re going to break down what this means for you.

Keeping track of what you sell and what you spend is also important. Accurate records make tax time a breeze. Also, some of the costs of running your eBay store can actually save you money on taxes. We’ll go over all these points, making them simple to understand.

Understanding Sales Tax Requirements for Online Sales

Sales tax is that extra bit of money buyers pay when purchasing something. You must know when and how to handle this tax.

Each state has its own rules about sales tax. Some states require you to collect sales tax on items you sell online, especially if you’re selling to someone in the same state.

Here’s how it works: if your state says you need to collect sales tax, you add a little extra to the sale price. This extra is the sales tax. You don’t keep this money. Instead, you send it to your state’s tax department at certain times during the year.

eBay can actually help with this. They have tools that automatically add the right amount of sales tax to your sales based on where your buyer lives. This makes it easier for you to follow the rules without having to figure out each state’s tax rate yourself.

Also, you can find all sorts of information on eBay’s Tax Information Center, so be sure to check it out. Keeping up with the right info helps you follow all the rules and avoid problems.

Navigating Income Tax for eBay Businesses

When you sell on eBay, the money you make isn’t just yours to keep straight away. Part of it might need to go to income tax.

Think of income tax as the part of your earnings you share with the government. It’s based on how much money you make from selling things.

Figuring out income tax starts with knowing your profits. Profit is what you have left after you subtract the cost of what you’re selling and any expenses from how much you sell it for. Expenses can include things like shipping costs, eBay fees, and the price you paid for what you sold.

You only pay income tax on your profits, not every dollar you make. This is why keeping track of your sales and costs is super important. It helps you see exactly how much profit you’re making.

If you’re making a good amount of money on eBay, the government considers you a business. This means you’ll need to report your earnings when tax time comes around. The good news is that you might also get to deduct some of your business costs.

Deductible Expenses for eBay Sellers

Think of eBay seller tax deductions as certain costs that can reduce how much tax you have to pay. It’s like getting a discount on your tax bill for the money you’ve spent running your eBay store.

Costs like buying inventory are deductible. This means when you buy something to sell on eBay, you can subtract that cost from your income, lowering the amount of tax you owe.

Don’t forget about shipping costs. The money you spend on boxes, packing materials, and even the postage for shipping items to your customers can be deducted, too.

For many eBay sellers, your home doubles as your office. A portion of your home expenses, like rent or mortgage and utilities, might be deductible if you use part of your home exclusively for your business.

Remember, keeping good records of these expenses is crucial. Hold onto receipts and make a note of each purchase related to your eBay business. This organization helps ensure you don’t miss out on any savings.

Sales Tax Nexus: What eBay Sellers Need to Know

Nexus means link or connection. In terms of sales tax, it refers to your business having enough of a presence in a state that the state says, “Hey, you need to collect tax from buyers here.”

You might create a nexus by having something physical like a store or warehouse in a state. But it can also happen if you sell a lot online to customers in a particular state. This “lot” varies by state. It could mean selling over a certain amount of money or a specific number of transactions in a year.

Knowing if you have a nexus in a state helps you figure out where you need to collect sales tax. Each state has its own rules, so a nexus in one state might not mean the same in another.

Luckily, eBay provides tools and resources to help you understand your nexus. They can automatically calculate if you must collect sales tax based on your sales patterns. If you’re having trouble finding what you need, the eBay Help and Contact section is a great place to get assistance.

The Importance of Keeping Accurate Records

Accurate record-keeping involves tracking every sale, noting expenses, and saving every receipt. This practice lets you understand your financial health by clearly showing your income and where your money is spent.

It’s crucial for calculating your profits accurately and ensuring you claim all possible deductions during tax time. Good records also simplify filling out tax forms by providing all the necessary information at your fingertips.

Furthermore, saved receipts serve as evidence for your financial transactions, offering security in case of audits. Start maintaining your records properly from now, and it will significantly benefit you in the future.

And that’s a wrap! We hope this guide has made your tax duties as an eBay seller clearer. Remember, it’s important to always stay up-to-date with tax information. If you’re ever unsure, double-check the details and make sure you’re following the rules. We wish you great success with your business!

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.